A Comprehensive Review of the Besqala Mining Valley Special Crypto Mining Zone

On April 17, 2026, the President of Uzbekistan signed Resolution No. PQ-143, establishing the Besqala Mining Valley special crypto mining zone and offering lawful mining enterprises tax exemptions for up to ten years. The resolution entered into force on April 20, 2026. Under the resolution, mining income generated within the special zone may be exempt from income tax, value-added tax and other major taxes until January 1, 2035, while enterprises are only required to pay a monthly administrative fee equal to 1% of mining revenue. After the resolution was signed, the relevant authorities were also required to submit amendments to the Tax Code so that the supporting tax regime could be synchronized with the new policy framework.

For mining enterprises that are reallocating computing power and energy resources globally, the Besqala Mining Valley special crypto mining zone is undoubtedly highly attractive. In recent years, the global crypto mining industry has continued to face rising electricity costs, tighter regulation and geopolitical shifts. For example, certain U.S. states have begun to strengthen grid oversight and environmental review; Kazakhstan gradually increased the tax burden on mining after experiencing power shortages; and Russia has been affected by international sanctions and restrictions on cross-border settlement. Against this backdrop, can Uzbekistan’s Besqala special mining zone, supported by long-term tax incentives dedicated to mining, become a potential dark horse for crypto mining enterprises seeking to expand into Central Asia? How can investors make flexible use of this policy dividend while effectively controlling potential tax and compliance risks? This article provides a comprehensive analysis of the special mining zone and its tax incentives by reference to policy texts, regional comparisons and investment risks.

Cryptocurrency mining is a typical power-intensive, computing-intensive and capital-intensive industry. For large mining farms at the level of several hundred megawatts, if they operate at high load over the long term, annual electricity consumption can be equivalent to that of hundreds of thousands of households. The purchase of mining machines, construction of power infrastructure and ongoing operations and maintenance may also generate capital expenditures at the level of hundreds of millions of U.S. dollars. Because mining costs are highly correlated with electricity prices, equipment efficiency and regulatory and tax arrangements, mining projects are usually highly sensitive to electricity prices, tax burdens and policy stability. Differences among jurisdictions in energy conditions and policy environments directly affect the distribution of industry profits, thereby driving global competition for hashrate resources. As competition intensifies, some emerging-market countries with abundant energy resources and a need for economic diversification have begun to attract crypto mining clusters by establishing dedicated zones or launching targeted policies, while also strengthening regulatory effectiveness.

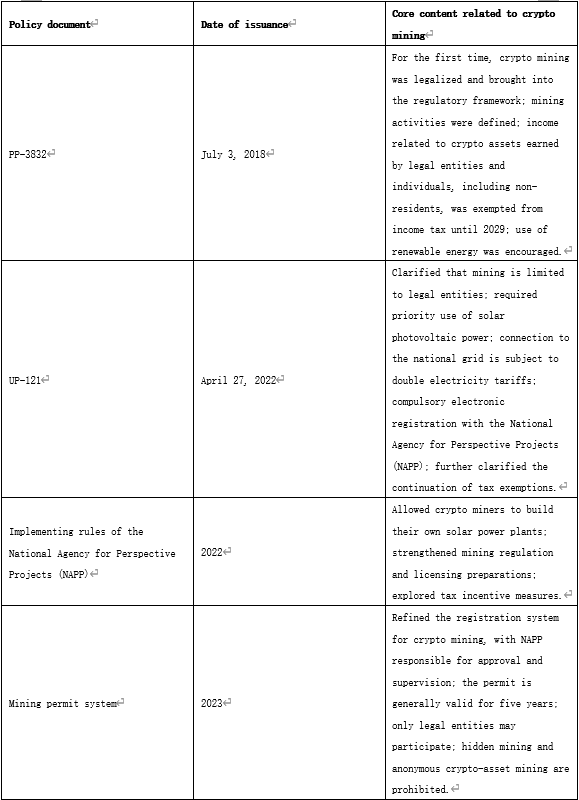

The evolution of Uzbekistan’s crypto mining policy is also related to these broader trends. Since Presidential Resolution No. PP-3832 in 2018 first permitted solar-powered mining, Uzbekistan has gradually liberalized its crypto mining industry: in 2018 it exempted income from crypto assets from income tax; in 2023 it refined the compulsory registration system for mining; in 2025 Presidential Decree No. PF-189 provided comprehensive incentive policies for large-scale crypto mining infrastructure projects in designated regions; and in April 2026 Presidential Resolution No. PQ-143 formally established the Besqala special mining zone and introduced a long-term ten-year tax exemption. Uzbekistan’s establishment of the special mining zone and tax incentives is intended to bring previously scattered mining activities into a unified regulatory framework. Specifically, the preferential policy will, on the one hand, enhance the investment attractiveness of the region and drive the construction of renewable energy infrastructure. On the other hand, through a unified electricity metering system, it will effectively reduce gray hashrate, disorderly electricity consumption and compliance risks, thereby improving regional economic competitiveness while safeguarding energy security and the healthy development of the industry.

Table 1 Evolution of Uzbekistan’s crypto mining policy

Unlike many countries that attract crypto mining enterprises merely through tax reductions or exemptions, Uzbekistan has introduced long-term tax incentives together with the establishment of a special mining zone. In nature, the special mining zone is a dedicated industrial-zone arrangement for the specific sector of cryptocurrency mining. By clustering similar mining enterprises in a concentrated physical space, it seeks to create economies of scale, facilitate unified management by regulators and coordinate energy allocation within the mining zone. This model is different from general nationwide tax incentives and also distinct from the traditional free economic zone policies usually designed for manufacturing. It is a sector-specific institutional arrangement introduced by Uzbekistan for the development needs of the digital-asset industry and targeted at the crypto mining sector.

The admission system of the Besqala special mining zone reflects the dual orientation of encouraging compliant investment while strictly preventing risks. By setting relatively high entry thresholds (Article 10 of Presidential Resolution No. PQ-143 and Annex 1) and a one-stop approval process, the regime screens institutions with genuine investment capacity and long-term operating intent, while bringing mining activities fully within regulatory oversight.

According to Presidential Resolution No. PQ-143, the special mining zone is located in the Republic of Karakalpakstan, the only autonomous republic within Uzbekistan. The region enjoys a high degree of autonomy and has long been one of the relatively less developed regions of Uzbekistan. In recent years, Uzbekistan has therefore continued to promote industrial transformation and economic revitalization in the region through new energy, the digital economy and special industrial parks. From the perspective of resource endowment, Karakalpakstan has extensive land resources and a relatively low population density. It has spatial conditions suitable for the development of large-scale energy infrastructure and centralized mining farms, and is also more suitable for hosting energy-intensive data centers and crypto mining operations.

In terms of regulatory mechanism, while establishing the special mining zone, Article 4 of Resolution No. PQ-143 expressly establishes the “Directorate of the Besqala Special Mining Zone” (the “Directorate”) as the local administrative body. The Directorate is founded by the Council of Ministers of the Republic of Karakalpakstan as the initiator, established in the form of a limited liability company, and directly subordinate to the regional government. It is responsible for the day-to-day management and operation of the special mining zone. Specifically, its main responsibilities include:

In addition to the Directorate, the National Agency for Perspective Projects (“NAPP” or the “Agency”) is designated as the exclusive authority for issuing permits for mining activities in the special mining zone. NAPP was established in 2017 and, institutionally, reports directly to the Office of the President of Uzbekistan. It is responsible for regulating the crypto-asset sector, including formulating crypto-asset-related policies and issuing permits. NAPP’s regulatory functions in the special mining zone include the following:

Overall, the local Directorate of the special mining zone is responsible for admission and day-to-day management, while central-level NAPP is responsible for licensing and specialized regulation. This creates a two-tier regulatory architecture that both leverages the initiative of the local government and ensures unified national regulatory standards for the crypto mining industry.

The special mining zone is open only to legal entities; natural persons may not directly participate in mining activities. Applicant enterprises must satisfy the following core conditions:

To safeguard energy security and operational regularity, applicant enterprises must focus on satisfying the following requirements:

In addition to the admission conditions described above, the special mining zone regime introduces a series of ongoing and mandatory compliance obligations, bringing mining activities into a dynamic regulatory system. Although these requirements do not constitute admission thresholds in the strict sense, they are statutory obligations that enterprises must perform continuously after being approved to enter the special mining zone. They therefore form an extension and important component of the admission system. These mandatory compliance obligations mainly include:

The core highlight of Presidential Resolution No. PQ-143 is its highly competitive long-term tax incentive policy. According to the resolution, lawful entities approved to conduct mining activities in the special mining zone may enjoy exemptions from taxes related to income derived from mining activities until January 1, 2035. This means that crypto mining enterprises in the special mining zone can obtain nearly ten years of stable expectations for a low tax burden. However, the special mining zone is not a zero-cost tax-exempt area in the absolute sense. The resolution also provides that the above-mentioned entities must pay the Directorate a monthly fee equal to 1% of the revenue derived from mining activities, and the net profit of the mining-zone Directorate will be transferred to the republican budget of the Republic of Karakalpakstan.

From an institutional-design perspective, the policy exempts corporate income tax while charging a 1% administrative fee on mining revenue. This creates a simplified collection model different from traditional profit-based corporate income tax. Under this model, enterprises no longer need to perform complex profit calculations, deductions, loss carryforwards and similar operations; instead, they pay a fixed percentage based directly on gross revenue. The government also avoids reviewing complex cost deductions, thereby reducing the cost of tax administration. A similar institutional logic can also be seen in tax policies of economic zones in emerging jurisdictions such as the United Arab Emirates, where qualified enterprises are exempt from income tax while being required to pay license fees, zone management fees and other administrative charges. This tax model has some appeal for industries with high capital investment and initial losses but large revenue scale, and may also help regions quickly form industrial clusters. It is also worth noting that neighboring Kazakhstan adopts a tax model for crypto mining that combines general income tax with fees based on electricity consumption. By comparison, Uzbekistan’s long-term exemption for income-related taxes and its retention only of a special fee equal to 1% of revenue indicate that it is currently more inclined to attract mining capital into the special mining zone through an ultra-low-tax approach.

In addition to tax incentives, Presidential Resolution No. PQ-143 provides supporting arrangements for the operation of the special mining zone, covering energy supply, electricity metering, infrastructure support, revenue settlement and management of major projects. These arrangements include both supportive conditions for mining-zone operations and regulatory requirements relating to energy use, capital repatriation and industrial activities, reflecting Uzbekistan’s attempt to strike an institutional balance between industrial development and national regulation. Among these arrangements, the energy-supply and electricity-management mechanisms form the core of the special mining zone’s operating system.

Before the establishment of the special mining zone, Uzbekistan imposed strict restrictions on electricity use for cryptocurrency mining. Under Presidential Resolution No. PQ-3832 of 2018 and the supporting rules of the administrative authority, cryptocurrency mining activities in the country were required to:

The above rules substantially raised entry thresholds and operating costs for the industry, limiting industry development to small- and medium-sized solar-powered projects and making large-scale commercial operation difficult. Therefore, in the electricity policy for the special mining zone, Presidential Resolution No. PQ-143 relaxes the above restrictions to a certain extent:

Compared with the earlier strict model that limited energy sources to solar power and imposed double tariffs, Presidential Resolution No. PQ-143 does not fundamentally change Uzbekistan’s cautious regulatory logic toward energy-intensive digital mining. Instead, while relaxing energy-source restrictions to a certain extent, it continues to control the impact of mining activities on the public grid through double tariffs, unified metering and centralized management. This institutional design also reflects Uzbekistan’s absorption of lessons from neighboring countries. Kazakhstan, for example, previously experienced power shortages, winter power rationing and expansion of illegal mining after large numbers of mining farms connected to the public grid. Against this background, Uzbekistan has not adopted a fully liberalized low-price electricity model. Instead, it uses high double tariffs to guide green-power construction and establishes a special zone for centralized management, seeking a balance between attracting digital-industry investment and maintaining domestic energy security.

In terms of the actual electricity price level, the cost of mining in Uzbekistan remains relatively high for enterprises connected to the national unified grid. Based on the second-category tariff group of approximately UZS 1,100/kWh, including VAT, applicable from June 1 of this year, the double tariff would require mining enterprises to pay approximately UZS 2,200/kWh, and additional peak-hour surcharges may apply. For mining farms operating under sustained high load, this still creates significant electricity-cost pressure. Therefore, although Resolution No. 143 relaxes restrictions on energy sources and allows continued grid supply to the mining zone, the policy design in practice still uses pricing mechanisms to guide mining enterprises toward self-built renewable energy and captive power plants. In particular, the permission to use abandoned oil and gas facilities to build supporting power-generation projects indicates that Uzbekistan is attempting to use demand from crypto mining to promote new-energy investment, energy development in remote regions and the reuse of stranded or abandoned energy resources, gradually linking crypto mining with energy-infrastructure construction and regional development policy. In the future, the development direction of Uzbekistan’s crypto mining industry is likely not large-scale reliance on the public grid, but the gradual formation of an industrial structure based on self-built renewable-energy power stations supporting crypto mining.

Under Presidential Resolution No. PQ-3832 of 2018 and NAPP’s subsequent supporting rules, mining activities conducted nationwide must install separate electricity metering devices if they are connected to the national unified power system, and must ensure that the metering equipment can be connected to the automated electricity metering and control system. Presidential Resolution No. PQ-143 continues these requirements and introduces no relaxation of metering standards. It requires enterprises in the special mining zone, when connected to the unified power system, to continue installing independent electricity metering devices that are compatible with and connected to the national automated electricity metering and control system.

The core purpose of this metering requirement is to maintain the security of the national grid. Because digital mining is a continuous, high-load industry, without real-time monitoring it can easily affect local grid stability and residential and industrial electricity use. The state therefore needs to dynamically understand the scale of mining-zone electricity consumption and changes in load through an automated metering system. Second, this regime is an important technical basis for implementing special electricity tariffs. Uzbekistan applies differentiated charging mechanisms such as double tariffs and peak-hour surcharges for mining, and independent metering ensures that mining electricity is distinguished from ordinary industrial, commercial or residential electricity, thereby ensuring accurate implementation of the special tariff regime. Third, the automated electricity metering and control system also plays an important role in combating illegal mining. By connecting mining operations to the national automated monitoring system, regulators can identify abnormal loads, unregistered mining farms and illegal connections, thereby reducing the impact of gray mining on the national grid and energy order.

Presidential Resolution No. PQ-143 makes targeted provisions on land-use facilitation and infrastructure support for the special mining zone, with a view to reducing investors’ upfront costs and accelerating project implementation:

Before the establishment of the special mining zone, Uzbekistan allowed crypto mining enterprises to sell crypto assets obtained from mining on domestic or foreign platforms, but sale proceeds, including income from conversion into other highly liquid crypto assets, were required to be settled and credited through the Uzbek domestic banking system. Resolution No. 143 continues and expressly strengthens this mechanism. Although resident enterprises in the special mining zone have the right to sell or exchange crypto assets obtained from mining on domestic crypto exchanges or foreign platforms, the sale proceeds must be mandatorily transferred into bank accounts within the Republic of Uzbekistan. This requirement applies to all sale and exchange proceeds. After mining proceeds are repatriated to domestic Uzbek banks, foreign-invested enterprises may apply for currency conversion and remit profits abroad in accordance with foreign-exchange administration rules.

While substantially opening mining activities and granting tax incentives, this foreign-exchange repatriation mechanism ensures that foreign-exchange income remains in the country and supports the economic development of the Karakalpakstan region. It also strengthens financial regulation and mitigates money-laundering risks by facilitating the tracing of capital flows.

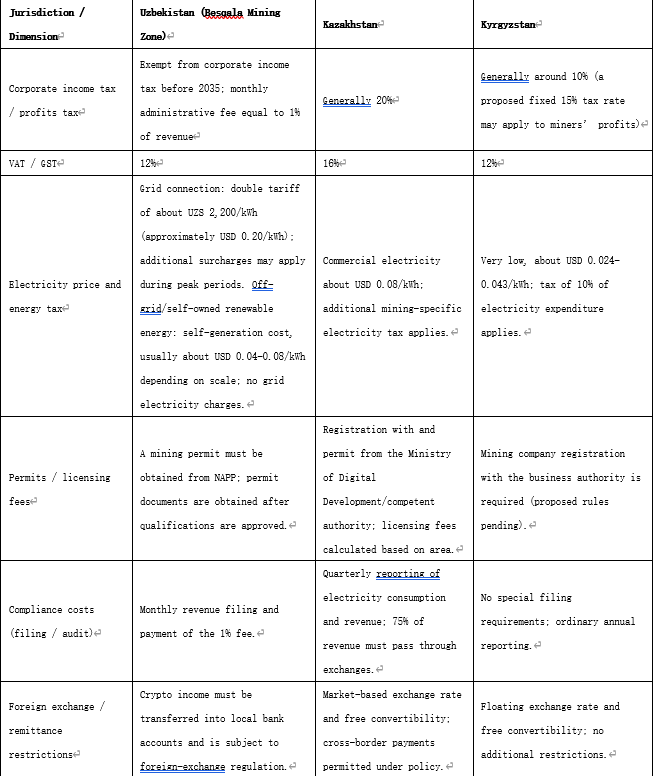

Looking only at a single tax rate is not sufficient to reflect the real tax burden of a region. The operating cost of a mining project is often affected by multiple factors, including corporate income tax, value-added tax, electricity prices and energy surcharges, licensing and filing requirements, day-to-day compliance costs and foreign-exchange settlement restrictions. On this basis, the following section horizontally compares Uzbekistan with Kazakhstan, Kyrgyzstan, Russia and other major neighboring markets across several dimensions, including tax burden, energy cost, admission thresholds, compliance requirements and capital repatriation, in order to more comprehensively identify the tax-burden competitiveness of Uzbekistan’s special mining zone.

Table 2 Comparison of tax policies in Uzbekistan and neighboring regions

The comparison shows that the advantages of Uzbekistan’s special mining zone lie not only in long-term tax exemption, but also in providing relatively stable expectations for investors. At the same time, its electricity price level, foreign-exchange repatriation arrangements and certain compliance requirements will also have a significant impact on the actual returns of projects. Compared with low-electricity-price markets such as Kazakhstan and Kyrgyzstan, Uzbekistan may not have an energy-cost advantage. However, compared with markets such as Russia, where tax burdens and compliance requirements are more complex, its dedicated policy arrangements have a certain degree of stability and operability. In subsequent project assessments, investors still need to conduct further calculations of comprehensive tax burden and profitability based on installed capacity, electricity-use structure and crypto-asset price volatility.

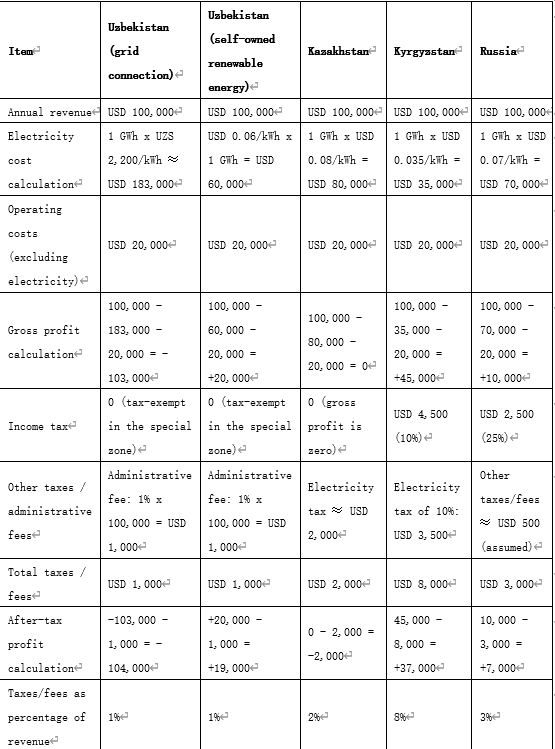

Based on the horizontal comparison of each country’s tax regime, electricity price level and compliance requirements above, it remains difficult to intuitively reflect the actual impact of different policy combinations on project profitability by looking only at institutional texts. For mining businesses, electricity cost usually accounts for the core portion of operating costs, while tax-fee structures, administrative fees and additional energy taxes further affect final after-tax returns. Therefore, under unified assumptions, a scenario-based calculation of comprehensive tax burdens and profitability across countries can more intuitively show the actual operational impact of the special mining zone policy:

Assumptions for the example: annual electricity consumption of 1 GWh (one million kWh); comprehensive self-owned renewable-energy supply cost of USD 0.06/kWh; annual mining output value equivalent to USD 100,000, corresponding to approximately USD 0.10/kWh in gross revenue; other operating costs excluding electricity of USD 20,000; and reference exchange rate of USD 1 approximately equal to UZS 12,000.

The above calculation shows that, under unified revenue assumptions, electricity price remains the core factor determining the profitability of mining projects, and its effect is clearly greater than that of corporate income tax and other taxes and fees themselves. Even if a project enjoys corporate income tax exemption in Uzbekistan’s special mining zone, if it is connected to the national grid, the project may face substantial overall losses under the current high electricity-price conditions. By contrast, under a self-owned renewable-energy supply model, because electricity cost falls significantly, project profitability would still improve markedly even after payment of a certain administrative fee.

However, it should be noted that the advantage brought by low electricity prices can easily be offset by a higher comprehensive tax burden, so the combined impact of electricity costs and tax-fee structures must be balanced. Although Kyrgyzstan has the lowest electricity price, it must pay both a 10% corporate income tax and a 10% special tax on electricity costs, significantly raising the comprehensive tax burden. As a result, although its after-tax profit remains positive, it does not show an outstanding advantage among the countries compared. Kazakhstan is similar. Although its corporate income tax rate is not particularly high, the additional electricity tax weakens its cost competitiveness.

Although Uzbekistan’s special mining zone has created a certain attraction for the crypto-asset mining industry through tax reductions and exemptions, crypto-asset mining itself is characterized by high energy consumption, high capital investment and strong regulatory sensitivity. Therefore, whether a crypto mining project has real investment value still requires a comprehensive assessment of energy costs, investor suitability and long-term compliance risks.

First, compared with the ten-year tax exemption, investors should place greater emphasis on electricity prices and the cost of building renewable-energy generation facilities. Although the special mining zone exempts mining income tax until 2035 and charges only an administrative fee equal to 1% of revenue, this also makes energy cost highly likely to become the largest operating expenditure for mining projects. On the one hand, connection to the national unified grid requires payment of double electricity tariffs (currently about UZS 2,200/kWh, equivalent to approximately USD 0.20/kWh), under which scenario projects are highly prone to losses. On the other hand, although the policy encourages the use of self-owned renewable energy, building new-energy power stations requires high upfront capital expenditures, including equipment procurement, land, energy-storage systems and grid-connection facilities. It also involves longer construction cycles and is significantly affected by local arid climate and resource conditions, which may influence overall project returns. Accordingly, the practical effect of the tax incentive will depend heavily on investors’ technical and financial strength in the new-energy sector.

Second, not all investors are suitable for entering the Besqala special mining zone. The zone sets relatively high entry thresholds for participants, and the double grid tariff and renewable-energy power-station construction requirements mentioned above further require investors to have strong financial capacity. Therefore, the special zone is more suitable for large institutional investors with renewable-energy development experience, “energy + mining” consortiums, large-scale investment projects, international mining companies with strong compliance capability and banking-access capability, and strategic investors willing to make a long-term commitment to the Karakalpakstan region and accept strict regulation. By contrast, small and medium-sized investors or purely financial investors that lack renewable-energy power-station construction and operating capabilities will have obviously insufficient competitiveness in the region and face higher entry barriers.

Third, mining within the zone involves certain compliance and operational risks. The special zone requires all mining proceeds to be transferred into bank accounts within Uzbekistan and be subject to foreign-exchange administration review. Although profit remittance is permitted, the requirement increases exchange costs, processing time and approval procedures, creating certain capital-repatriation risk. At the same time, projects must install independent electricity metering devices and connect them to the national automated metering and control system, file monthly revenue reports and pay the 1% administrative fee. Failure to comply strictly may give rise to regulatory compliance risks. In addition, although the tax incentive period extends to 2035, uncertainties remain regarding the pace of subsequent implementing rules, the stability of power supply and the level of local-government support. Geopolitical risks, fluctuations in Bitcoin prices and network difficulty, and the relatively weak power and internet infrastructure in Karakalpakstan may also challenge long-term project operations.

Overall, the Besqala special mining zone provides a rare policy window in Central Asia for large professional investors with renewable-energy development capability and long-term compliance intent. However, for small and medium-sized investors or projects that rely purely on the grid, risks remain relatively high. Potential investors are advised to conduct detailed due diligence before entry and jointly assess project feasibility with local partners or professional legal advisers.

With the ten-year tax exemption policy introduced under Presidential Resolution No. PQ-143, Uzbekistan’s Besqala special mining zone provides a new and attractive Central Asian option for global crypto mining enterprises. However, the practical effectiveness of the policy depends heavily on whether investors can effectively control energy costs and possess renewable-energy development capabilities. Under a self-owned renewable-energy model, the special zone is significantly competitive, whereas small and medium-sized investors that connect to the grid or lack energy-development capability face relatively high risks. Overall, the Besqala special mining zone is more suitable for large professional institutions with financial strength, renewable-energy development experience and long-term compliance intent. For such strategic investors, it is likely to become a potential destination in Central Asia that deserves close attention.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.