In 2026, tokenized U.S. stocks seemed to move almost overnight from small-scale pilot projects to a new entry point being pursued by major exchanges. On May 26, Bitget officially launched Reality, its RWA platform, and brought rToken, a tokenized U.S. stock product, to the market. Bybit and other platforms had earlier integrated xStocks, allowing users to trade certain tokenized stocks within their exchange accounts. Robinhood has also launched a range of tokenized U.S. stock and ETF products for EU users and plans to support more RWA use cases through its own Layer 2 blockchain.

As exchanges move into the U.S. stock tokenization market, the tokenized U.S. stock narrative has become increasingly popular. Stocks and ETFs are becoming one of the more imaginative directions for the next stage of the RWA sector. Buying an on-chain token that tracks the price of Nvidia, Tesla, or an S&P 500 ETF is far more intuitive than trying to understand complex on-chain yield structures. This gives tokenized U.S. stocks natural retail recognition and trading demand.

When we shift the focus from exchanges to a broader investor base, this emerging investment market represents broad opportunities, while also bringing doubts and risks caused by information asymmetry. What exactly are the products commonly referred to as tokenized U.S. stocks? What is their legal nature? Do gains from investing in tokenized U.S. stocks need to be taxed? How should tax planning be carried out? The following sections will systematically break down the definition and structure of U.S. stock tokenization around the main issues that investors care about, and will briefly analyze the potential tax planning issues involved.

The term tokenized U.S. stocks, as commonly used in the market, is not a strict legal concept. More precisely, it usually refers to a category of financial instruments that use U.S.-listed stocks, ETFs, or related equity assets as reference assets, and provide investors with tradable economic exposure, income distributions, or entitlement certificates through on-chain tokens or smart contract structures.

Here, it is important to distinguish between a stock itself and economic exposure to a stock. In traditional U.S. stock investment, investors generally hold shares either as registered shareholders or as beneficial owners under a brokerage account. Tokenized U.S. stock products usually package only part of those economic rights into tokens. Investors mainly obtain exposure to price movements. Some products arrange dividend mapping or redemption mechanisms, but this does not automatically mean that holders receive full shareholder rights. In other words, what investors buy may not necessarily be the stock itself. It may instead be a contractual claim against the issuer, a certificate of beneficial interest, or a synthetic asset that simply tracks price movements.

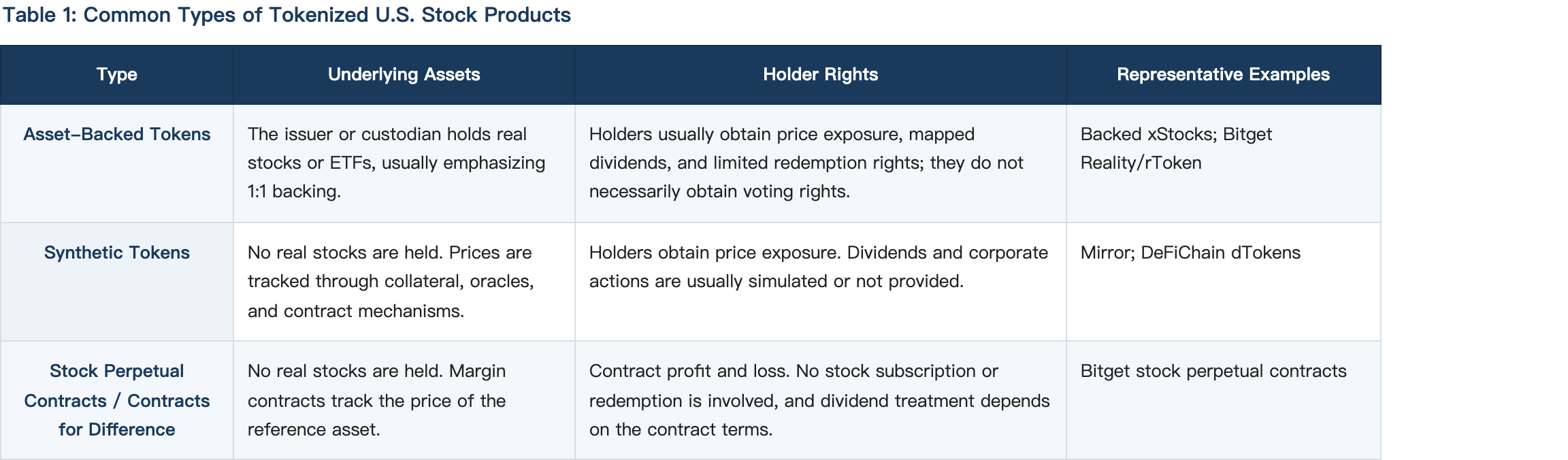

Based on publicly available project materials and market practice, current tokenized U.S. stock products can be divided into at least three categories: asset-backed tokens, synthetic tokens, and stock perpetual contracts or contracts for difference.

Asset-backed tokens are the model closest to the original meaning of stock tokenization. The core structure is that the issuer or its partner custodian holds real U.S. stocks or ETFs in the traditional securities market, and then issues on-chain tokens corresponding to the underlying assets. Ideally, each token is backed by a corresponding proportion of real stock or ETF reserves. After holding the token, users can gain exposure to price movements of the underlying asset and, where the product rules allow, receive rights such as mapped dividends.

This model can be further divided into third-party issuance and platform self-issuance. Under the third-party issuance model, the tokens are issued by an external institution, while exchanges mainly handle product integration and distribution. Users can select tokens directly within the exchange system in one place. Taking xStocks as an example, Backed Finance, as the issuer, uses stocks and ETFs as reserves, deploys the corresponding tokens on Solana, and relies on platforms such as Bitget and Kraken for distribution and trading access.

Under the platform self-issuance model, token design, custody arrangements, and other issuance activities are directly handled by the exchange or its affiliated platform. For example, in Bitget’s Reality/rToken product, the platform states that each rToken is backed by real stocks held with a U.S. broker. The issuer works with licensed brokers connected to Nasdaq and the New York Stock Exchange, and uses an independent third-party institution to provide proof of reserves, with the reserve ratio maintained above 100%. Reality converts corporate dividends into stablecoins (USDT) and distributes them directly to holders, while stock splits and reverse stock splits are automatically reflected in rToken balances.

Synthetic tokens are not directly linked to real stocks. Instead, they use smart contracts, collateral, or oracle-based pricing mechanisms to simulate the price performance of a particular stock or ETF. After users buy this type of token, they are essentially obtaining an on-chain synthetic exposure that tracks the price of U.S. stocks, rather than holding an entitlement certificate backed by real stocks. Early products such as Mirror Protocol and DeFiChain dTokens had this feature.

The advantage of synthetic tokens is that they can scale more quickly, because they do not require real stock custody and securities brokerage arrangements for every reference asset. As long as prices can be provided and sufficient collateralization can be maintained, multiple stock price exposures can theoretically be generated. But the risks of this structure are also more obvious. Once the market fluctuates sharply or collateral becomes insufficient, the token price may depeg from the target stock or ETF price. Compared with asset-backed tokens, synthetic tokens are closer to on-chain price derivatives than to tokenized stocks in the strict sense.

Stock perpetual contracts or contracts for difference are another type of product that is often included in discussions of tokenized U.S. stocks. They usually do not hold real stocks and do not issue tokens representing rights to the underlying securities. Instead, they use stablecoins as margin and track the price movements of a stock or ETF through contract arrangements. Users trade long and short positions and profit-and-loss differences, rather than the stock itself. Typical examples include Bitget’s USDT-margined stock perpetual contracts such as NVDAUSDT, TSLAUSDT, METAUSDT, and GOOGLUSDT.

Compared with other products, stock perpetual contract products are easier to launch because their logic is close to crypto perpetual contracts. The platform provides a price index and sets margin rules, funding rates, and liquidation mechanisms, while users open positions with USDT or USDC to trade price movements of U.S. stock reference assets. Stock perpetual contracts are efficient to trade, allow both long and short positions, support leverage, and do not require complex stock subscription, redemption, or dividend distribution arrangements. They do not provide ownership of the underlying stocks and do not promise corresponding real stock reserves.

Table 1: Common Types of Tokenized U.S. Stock Products

As noted above, tokenized U.S. stocks actually include several types of products with very different legal characteristics. From asset-backed tokens to U.S. stock-linked perpetual contracts and synthetic assets, different products have their own features in terms of tax characterization and compliance requirements.

Taking asset-backed U.S. stock tokens as an example, the operation of the project involves multiple steps, including holding the underlying shares, token issuance and custody, and the holding and transfer of tokens. Under U.S. tax law, the entity that holds the underlying shares, such as a U.S. broker acting as the registered shareholder, has withholding tax obligations under Sections 1441 and 1442 of the Internal Revenue Code for dividends generated, and in principle should withhold 30% or the applicable treaty rate on dividends paid to non-U.S. beneficial owners. For the token issuer, if holders of the product legally have a contractual claim against the issuer, and if the token or related contract is characterized under U.S. tax law as a specified notional principal contract (specified NPC), specified equity-linked instrument (specified ELI), or another substantially similar arrangement linked to U.S. stocks, and if dividend equivalents are paid to or embedded for non-U.S. holders, the issuer may become a new withholding agent because it pays the dividend equivalent payment referred to in Section 871(m). At the same time, gains and losses from stock perpetual contracts are treated in most jurisdictions as gains and losses from derivative transactions and do not involve dividends. In principle, they do not trigger traditional dividend withholding under Section 871(m), unless the contract economically embeds or adjusts for U.S. stock dividends and is characterized as a Section 871(m) instrument with dividend equivalent features, which must be determined based on technical standards such as delta. In short, different types of products differ in tax characterization and treatment. Separately presenting perpetual contracts and asset-backed tokens in tax statements and tax documentation is an important way to reduce reporting classification errors.

The room for tax optimization in issuing and operating tokenized U.S. stock products lies within a compliant structure, including reducing duplicate reporting, clarifying the withholding agent, and applying tax treaties:

For individual investors, one major misconception about tokenized U.S. stocks is to treat on-chain holding as tax invisibility. As CARF and the amended CRS framework are gradually implemented, tax transparency for crypto-asset transactions and related financial accounts is increasing. In the EU, DAC8, as the EU’s local implementation of CARF, requires Member States to apply the relevant rules from January 1, 2026, and complete the first exchange of information for the first reporting year by September 30, 2027. Jurisdictions including the United Kingdom, the United States, and Hong Kong have also committed to implementing CARF and are making the corresponding legislative preparations.

In August 2022, the OECD completed amendments to the CRS framework, bringing specified electronic money products and central bank digital currencies into the reporting scope. The amended CRS mainly covers financial accounts and various indirect crypto-related transactions, including electronic money, central bank-issued digital currencies, and crypto-related exposure arising through derivatives or funds. CARF, by contrast, focuses on on-chain or crypto-related transactions and requires relevant institutions to report at the transaction level.

A more cautious understanding of the boundary between the two frameworks is that investing in tokenized U.S. stocks is not an either-or choice between CARF and CRS. Information at different layers may trigger different mechanisms. At the on-chain token layer, the platform, as a Reporting Crypto-Asset Service Provider (RCASP), is subject to CARF. The underlying U.S. brokerage account and users’ stablecoin and fiat balances may fall under CRS. These mechanisms may overlap within the same product. Specifically, attention should be paid to the following aspects:

Of course, whether these institutional principles ultimately apply to a specific taxpayer still depends on a series of practical conditions. For example, it depends on whether the jurisdiction where the exchange is located has implemented CARF, whether there is an activated exchange relationship between that jurisdiction and the user’s jurisdiction of tax residence, and how far the user’s jurisdiction has progressed in adopting the framework.

It should be noted that whether information can be automatically exchanged and whether the holder has a tax obligation under the tax law of their jurisdiction of residence are two separate issues. The latter is not eliminated simply because the former is absent. In other words, even if information on tokenized U.S. stock holdings is currently difficult to exchange automatically back to the jurisdiction of residence through CARF or CRS, the holder still has an obligation to voluntarily report and pay tax on the relevant foreign-source income, such as gains from property transfers and dividend income, under the domestic tax law of that jurisdiction.

Finally, on-chain invisibility is not the end of the story. The flow of funds will eventually return to the traditional financial system. When holders convert gains into fiat currency, move funds in or out through bank accounts, use the funds for real-world consumption, or purchase assets, these activities remain within the view of tax authorities and anti-money laundering regulators. The opacity created by on-chain holding will eventually be exposed again at the points where it touches the traditional financial system.

Market data show that tokenized U.S. stocks are still at an early stage of development, but their growth has already been fast enough to attract early positioning by exchanges and issuers. According to CoinGecko’s 2026 RWA report, the market capitalization of tokenized RWAs increased from USD 5.42 billion at the beginning of 2025 to USD 19.32 billion by the end of the first quarter of 2026, representing growth of 256.7% over 15 months. Tokenized stocks accounted for about 2.5% of the RWA market, while tokenized ETFs accounted for about 1.5%. Although this scale remains limited compared with the global equity market, it is enough to show that stocks and ETFs are gradually standing out from the RWA narrative and becoming a new entry point for trading platforms to compete over. For exchanges, the appeal of tokenized U.S. stocks is not limited to trading volume itself. Crypto spot trading, contracts, and other businesses are affected by market cycles, so exchanges need to introduce new tradable assets to expand revenue from trading, market making, custody, subscription and redemption, and structured products. For users, the advantages of tokenized U.S. stocks lie in small-ticket participation, extended trading hours, and near-real-time settlement.

Tokenized U.S. stocks may look like simply moving U.S. stocks onto the blockchain, but behind them is not a single product form. Instead, they involve multiple structures with different underlying assets and different holder rights. If investors simply understand all of them as U.S. stocks, they may underestimate product risks. If operators simply understand all of them as crypto-assets, they may overlook the compliance requirements created by underlying securities, dividend withholding, and related rules. For market participants, the opportunities brought by tokenized U.S. stocks deserve attention, but the tax and regulatory complexity of the products themselves should not be ignored. Only with a solid compliance mindset can participants move steadily as the RWA market enters deeper waters.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.