As the world's largest archipelagic country, Indonesia consists of over 17,500 islands spanning the Pacific and Indian Oceans, earning it the reputation of the "Country of a Thousand Islands." Indonesia holds a significant position in the cryptocurrency market. According to Chainalysis's 2025 Global Crypto Adoption Index, Indonesia ranks 7th globally, and it is also at the forefront in dimensions such as DeFi activities, centralized service usage, and institutional transactions. Against this backdrop, Indonesia has been continuously adjusting its regulatory and tax treatment of crypto assets in recent years. Under the newly promulgated Ministry of Finance Regulation No. 108 of 2025, Indonesia's Directorate General of Taxes (DGT) is now authorized to obtain account and transaction data directly from e-wallet, e-money, and cryptocurrency service providers, ensuring they fulfill the same data reporting obligations as traditional financial institutions. The continuous adjustments in Indonesia's tax arrangements and regulatory approaches to crypto assets have prompted crypto market participants to re-examine compliance requirements.

Based on this, this article will conduct a fundamental research on the overall framework of Indonesia's crypto asset tax system and regulatory framework, focusing on outlining its basic tax system, the tax treatment of crypto assets, the division of labor among regulatory authorities, and its core rules.

2.1 Overview of Indonesia's Tax System

Indonesia implements a two-tier taxation system at the central and local levels. Tax legislative and collection powers are primarily concentrated in the central government, while local governments have the authority to formulate certain local tax regulations. Indonesia has a comprehensive and diverse range of taxes, mainly including Corporate Income Tax, Personal Income Tax, Value Added Tax (VAT), Luxury Goods Sales Tax, Land and Building Tax, Stamp Duty, Entertainment Tax, Motor Vehicle Tax, and Advertising Tax. The core legal basis of Indonesia's tax system includes the Income Tax Law (ITL), the Value Added Tax on Goods and Services Law, the Luxury Goods Sales Tax Law, the General Provisions and Tax Procedures Law (GTL, Law No. 6 of 1983), and the Harmonization of Tax Regulations Law (UU HPP, Law No. 7 of 2021), which apply throughout the entire territory of Indonesia, including its exclusive economic zone and continental shelf.

2.2 Determination of Tax Residency

2.2.1 Resident Corporate Taxpayers

Any organization established in Indonesia or whose place of effective management is in Indonesia, except for certain government agencies meeting specific criteria, is considered a tax resident entity for tax purposes. To determine whether a foreign enterprise is recognized as a local tax resident, it is often necessary to evaluate based on both its place of incorporation and the location of its place of effective management.

According to the Indonesian Income Tax Law and the Indonesian Directorate General of Taxes Regulation No. 23 of 2025, a "resident corporate taxpayer" refers to an entity established or registered in Indonesia. The existence of any of the following circumstances is deemed as being registered in Indonesia: (1) The articles of association stipulate its place of registration as Indonesia; (2) Its headquarters, administrative center, or financial center office is located in Indonesia; (3) It has a controlling office in Indonesia responsible for management activities; (4) Board of directors meetings for strategic decision-making are held in Indonesia; (5) Its management members reside or are domiciled in Indonesia.

In short, even if an enterprise is not registered in Indonesia, it is still regarded as a tax resident if its place of effective management (also known as the "center of management and control") is located in Indonesia. The place of effective management refers to the location where strategic decisions and day-to-day operational decisions are actually made. Considerations include, but are not limited to, investment decisions, management appointments, board of directors meetings, dividend supervision, and financial control.

2.2.2 Resident Individual Taxpayers

Any individual who resides in Indonesia for more than 183 days in any consecutive 12-month period, or who resides in Indonesia and intends to remain there, is considered a resident taxpayer. According to Ministry of Finance Regulation No. 18 of 2021, an individual meeting any of the following conditions is considered an Indonesian resident individual: Residing in Indonesia, meaning having a permanent home, center of vital interests, or habitual abode in Indonesia; Residing in Indonesia for more than 183 days within any consecutive 12-month period; Residing in Indonesia during a tax year with the intention to remain (such intention to remain needs to be proven by documents such as a permanent residence permit, a limited stay visa or permit valid for more than 183 days, an employment or business contract with an implementation period exceeding 183 days, a lease contract exceeding 183 days, or information indicating the relocation of family members to Indonesia).

2.3 Common Taxes

2.3.1 Corporate Income Tax

Resident corporate taxpayers and permanent establishments (PEs) in Indonesia are subject to Corporate Income Tax on their income derived from both within and outside Indonesia, whereas non-resident enterprises are only subject to Corporate Income Tax on their income sourced within Indonesia. In terms of tax rates, the Corporate Income Tax rate for resident corporate taxpayers and permanent establishments is generally 22%, while non-resident enterprises that do not constitute a permanent establishment are typically subject to a 20% final withholding tax on their gross income sourced from Indonesia. Enterprises meeting certain specific conditions may enjoy preferential tax rates. For instance, resident corporate taxpayers with an annual gross income not exceeding IDR 50 billion are eligible for a 50% tax discount on the taxable income corresponding to the gross income portion up to IDR 4.8 billion. Furthermore, specific small and micro enterprises with an annual gross income not exceeding IDR 4.8 billion are subject to a final income tax calculated at 0.5% of their gross income.

Income tax in Indonesia is primarily levied in the form of withholding tax. For eight categories of income, including dividends, interest, royalties, service fees, and capital gains from property transfers, entities such as resident corporate taxpayers, government institutions, event organizers, permanent establishments, or representative offices of non-resident enterprises are required to withhold tax upon payment of the income.

2.3.2 Personal Income Tax

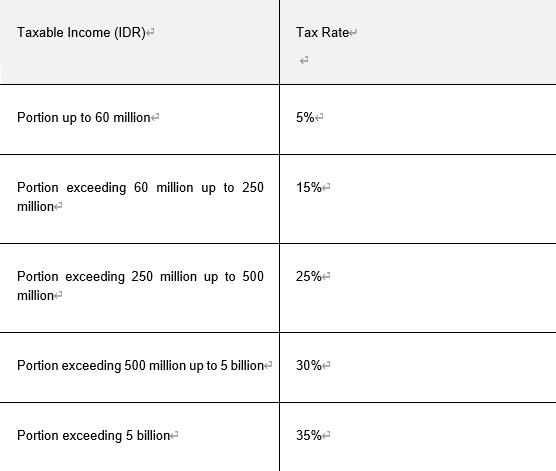

Resident individuals are subject to income tax on their worldwide income, including capital gains. Personal income tax generally applies a five-bracket progressive tax rate structure. Concurrently, resident taxpayers can enjoy tax benefits such as non-taxable income allowances, occupational expense deductions, pension contribution deductions, and donation deductions. Non-resident taxpayers are only taxed on income sourced from Indonesia and are subject to a flat final tax rate of 20%, without the ability to claim tax deductions, exemptions, or credits.

Table 1: Personal Income Tax Rates for Resident Individuals in Indonesia

2.3.3 Value Added Tax (VAT)

The liable subjects for VAT in Indonesia are individuals, enterprises, or government institutions that sell taxable goods or services. Offshore sellers, service providers, or e-commerce platforms meeting specific conditions will be designated as VAT collectors. Effective from January 1, 2025, the standard VAT rate in Indonesia is 12%, with an effective rate of 11%, and the applicable tax rate for different goods ranges from 5% to 15%. Specifically, for the import and delivery of luxury goods subject to Luxury Goods Sales Tax, the VAT rate is 12%; for other non-luxury goods, the tax is calculated as 11/12 of the import value, selling price, or compensation value, resulting in an effective VAT rate of 11%. Concurrently, a VAT exemption policy is implemented for basic necessities (such as rice and salt), medical and educational services, and financial services (such as loans and insurance), while the export of specific services or labor can enjoy a zero-rating.

3.1 Tax Classification of Crypto Assets

The legal and tax classification of crypto assets has undergone an evolutionary process from commodities to financial assets. As early as 2014, an official statement from Bank Indonesia (BI) clarified that virtual currencies are not legal tender and strictly prohibited their use as payment instruments, a stance reiterated in 2018. In 2022, Indonesia's Minister of Finance Regulation No. 68 (PMK 68/2022) stipulated that crypto assets are intangible commodities in digital form. With the enactment of Law No. 4 of 2023, crypto assets were reclassified as Digital Financial Assets (Aset Keuangan Digital), which was further clarified in Government Regulation No. 49 of 2024. In 2025, the Indonesian government issued Minister of Finance Regulation No. 50 (PMK 50/2025), which defines crypto assets as digital representations of value that can be electronically stored and transferred using distributed ledger technology (such as blockchain). These assets are not guaranteed by any central authority but are issued by private entities and can take the form of digital currencies, tokens, or other asset forms, including backed crypto-assets and unbacked crypto-assets.

The tax treatment of crypto assets in Indonesia mainly involves VAT and Income Tax, with the latter comprising final income tax and general income tax. In terms of VAT, the pure transfer of crypto assets is treated as the transfer of securities and is exempt from VAT; however, those involving the provision of crypto asset-related services (such as providing crypto trading platforms, wallets, etc.) are still subject to VAT. In terms of Income Tax, the income earned by sellers or miners of crypto assets is subject to income tax. Simply holding crypto assets, transferring crypto assets between wallets, or purchasing cryptocurrencies typically does not trigger a tax liability.

3.2 Tax Treatment in Different Scenarios

3.2.1 Transfer and Trading of Crypto Assets

The transfer and trading of crypto assets refer to the transfer and exchange of ownership of crypto assets, including purchasing crypto assets with fiat currency, exchanging crypto assets for one another (swapping), and other forms of crypto asset transactions.

For VAT treatment, the transfer of crypto assets itself does not require the payment of VAT, but platform services and miner verification services related to transactions may still constitute taxable services.

For Income Tax treatment, the revenue derived from selling crypto assets falls within the scope of income tax and is subject to the final income tax rules (PPh 22). The applicable tax rate depends on the type of Electronic System Trading Operator (PPMSE): (1) trading through general domestic PPMSEs is subject to a 0.21% final income tax, which is withheld, remitted, and reported by the PPMSE; (2) trading through domestic limited-service PPMSEs is subject to a 0.21% final income tax, which must be paid and reported by the seller themselves; (3) trading through designated foreign PPMSEs is subject to a 1% final income tax, which is withheld, remitted, and reported by the PPMSE; (4) trading through un-designated foreign PPMSEs is also subject to a 1% final income tax, but requires the seller to report and pay it themselves.

3.2.2 Provision of Services by Trading Platforms

This refers to the taxable services provided by PPMSEs (Penyelenggara Perdagangan Melalui Sistem Elektronik, or Electronic System Trading Operators), including the provision of electronic channel services for crypto asset trading, deposit and withdrawal services, crypto asset transfer services between e-wallets, the provision and management of crypto asset storage media or e-wallets, and other services related to crypto assets.

Regarding VAT, PPMSEs pay VAT on the crypto asset trading facility services they provide, calculated by multiplying a nominal rate of 12% by other tax bases, resulting in an actual effective tax rate of 11%. The PPMSE must declare this in its monthly VAT return.

Regarding Income Tax, the income derived by PPMSEs from providing crypto asset trading facilities and related services falls within the scope of income tax and is taxed at the general tax rate under the Income Tax Law (the general corporate income tax rate is 22%), and must be declared in the PPMSE's annual income tax return.

3.2.3 Miners Providing Transaction Verification Services and Conducting Mining Activities

The taxable services provided by crypto asset miners refer to the taxable services provided in the form of crypto asset transaction verification services, meaning that miners, through their computing power and technical capabilities, verify and confirm the validity of crypto asset transactions and record the transactions onto the blockchain network.

Currently, the applicable effective VAT rate is approximately 2.2% of the value of the crypto assets obtained by the crypto asset miner, and the tax base includes the block rewards received by the miner. The income obtained by miners through mining activities, including service remuneration, block rewards, transaction verification fees, other income obtained from the system, and other related income, is levied at the general rate of the Income Tax Law and must be declared in the miner's annual income tax return. If the miner subsequently sells the crypto assets as a seller through a PPMSE, the sales revenue is also subject to PPh 22 according to the seller's trading rules.

4.1 Regulatory Authorities and Their Division of Labor

In 2025, Indonesia carried out a major reform of its crypto asset regulatory framework, officially transferring the supervision and regulatory responsibilities for digital financial assets, including crypto assets and certain financial derivatives, from the Commodity Futures Trading Regulatory Agency (Bappebti) to the Financial Services Authority (OJK, Otoritas Jasa Keuangan) and Bank Indonesia (BI), thereby regulating crypto businesses alongside other financial services. This move marks the formation of a new landscape in Indonesia's crypto asset regulation. OJK has become the core regulatory authority for crypto assets in Indonesia, implementing specific supervision over the fintech, digital asset, and crypto asset sectors, with responsibilities covering rule-making, market access management, daily supervision, and risk resolution, while Bank Indonesia has taken over the regulatory responsibilities for financial derivatives related to the money market and foreign exchange market. Concurrently, as the tax collection agency under the Ministry of Finance, the Indonesian Ministry of Finance and the Directorate General of Taxes (DGT, Direktorat Jenderal Pajak) are responsible for the tax collection and administration of crypto asset transactions. With OJK at the core, and BI and DGT collaborating synergistically to perform their respective functions, they jointly construct the overall structure of Indonesia's crypto asset regulatory authorities.

4.2 Core Legal Framework and Regulatory Policies

Indonesia's current crypto asset regulatory framework can be summarized as a hierarchical structure, based on Law No. 4 of 2023 (UU P2SK) as the primary legal foundation, with OJK Regulation No. 27 of 2024 serving as the core rule, supplemented by other supporting regulations. On January 12, 2023, Indonesia enacted UU P2SK, which authorized the transfer of regulatory responsibilities for digital financial assets to financial regulatory authorities such as OJK and BI, marking the initial emergence of a paradigm shift in crypto assets from "commodity regulation" to "financial regulation."

To fulfill its duties, OJK issued Regulation No. 27 of 2024 (POJK 27/2024) in December 2024. This regulation revamped the original crypto asset regulatory rules, making systematic arrangements for institutional setup, licensing, governance, trading mechanisms, consumer protection, and personal data protection in accordance with financial service regulatory standards, thus becoming the new core regulatory rule. The regulation also identified four key participants in Indonesia's crypto asset trading ecosystem, including Digital Financial Asset (DFA) exchanges, DFA traders, clearing, guarantee, and settlement institutions for DFA transactions, and DFA custodians. As a supporting implementation document, OJK concurrently issued Circular Letter No. 20/SEOJK.07/2024, which provided specific operational guidance for crypto trading, detailing the license application process, business plan requirements, periodic reporting systems, and governance structure requirements. In 2025, OJK promulgated Regulation No. 23 of 2025 (POJK 23/2025), making significant amendments to POJK 27/2024. The focus was on expanding the regulatory scope of digital financial assets and filling the gaps in business specifications and risk control requirements concerning the regulation of crypto derivatives.

Overall, Indonesia's crypto asset regulation is shifting from a model previously dominated by commodity futures regulation to a digital financial asset regulatory framework centered around OJK. As POJK 23/2025 incorporates digital financial asset derivatives into the regulatory scope, and the authorities have committed to commence the Crypto-Asset Reporting Framework (CARF) information reporting starting from 2027, the compliance focus for crypto market participants in Indonesia has expanded from a singular trading license to multiple layers, including market access, trading governance, consumer protection, tax declaration, and cross-border information exchange.

As one of the critical economies in Southeast Asia, Indonesia's total crypto asset trading volume reached IDR 482.23 trillion in 2025, and the single-month trading volume in January 2026 reached IDR 29.24 trillion. The continuously growing trading scale fully reflects consumer confidence and market stability in the crypto asset sector within the Indonesian market. From a regulatory landscape centered around OJK with multi-departmental synergy involving BI, DGT, and others, to establishing a legal framework that transitions from commodity regulation to financial regulation, Indonesia strives to progressively build a digital financial asset governance system that aligns with its national conditions. The future of crypto assets in Indonesia remains full of variables. However, with the emergence of opportunities such as massive market demand, technological innovation, and international layout, whether this "Country of a Thousand Islands" can create sufficient development space for the crypto industry while maintaining regulatory prudence, thereby securing an advantageous position in the Web3 competition across Southeast Asia and globally, warrants continuous attention.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.