Over the past year, as tax authorities in multiple regions have successively issued declaration reminders to resident individuals receiving overseas income, and the Common Reporting Standard (CRS) information exchange has transitioned into normalized operation, the concept of "tax resident status" has begun to enter a broader public view. A frequently raised, yet often misunderstood question emerges: Based on what criteria is an individual or an enterprise ultimately determined to be a tax resident of a certain country or region? And why is this determination so crucial?

The determination of tax resident status lies at the starting point of cross-border tax issues; it determines the scope of tax obligations itself. For an individual, whether they constitute a Chinese tax resident determines whether their overseas income needs to be included in the taxation scope of China’s individual income tax; for an enterprise, resident status determines whether it needs to pay enterprise income tax in China on its global income or solely on its domestic income. Status determination precedes tax calculation and is the prerequisite for confirming the attribution of taxation rights.

This article takes the determination of tax resident status as the main thread, discussing four levels sequentially: the legal significance of status determination and three easily confused concepts; the criteria for determining an individual’s tax resident status, contrasting the rules of China and the United States; the criteria for determining the tax resident status of an enterprise (entity); and in the case of dual residency, how the tax treaty tie-breaker rules determine a single attribution. Finally, in combination with the background of CRS information transparency, it explains the practical significance of accurate status determination in the current compliance environment.

Tax law sets different scopes of tax obligations for residents and non-residents. A tax resident typically bears unlimited tax liability, meaning they are taxed on all their income sourced from both inside and outside the territory; a non-resident bears limited tax liability, meaning they are taxed only on income sourced from within the territory. The treatment of the exact same overseas income differs entirely under the two statuses of resident and non-resident, which is precisely why status determination is at the core.

In practical communication, the most common misunderstanding is equating tax resident status with nationality, or equating it with holding permanent residency in a certain location. These three are not concepts on the same level: nationality is a legal status as a national; the permanent right of residence (such as a U.S. Green Card or Hong Kong permanent resident status) is a residency qualification under immigration law; whereas tax resident status can only be judged independently based on the requirements of tax law regarding domicile and time of residence. Holding a long-term residence qualification in a certain place does not directly equate to constituting a tax resident in that place, and vice versa. Clarifying this distinction is the foundation for all subsequent determinations.

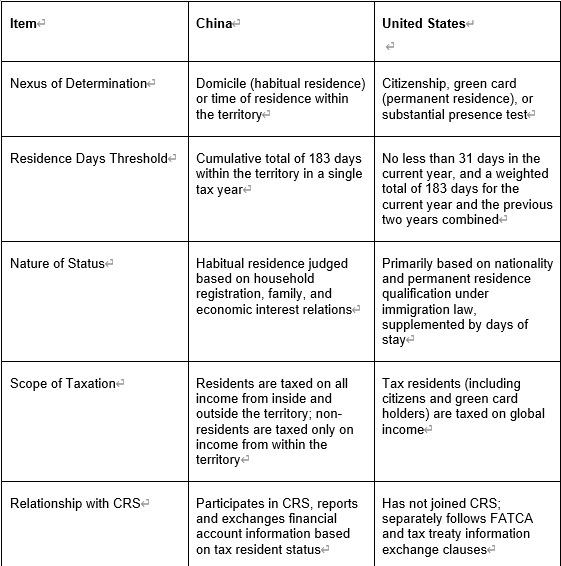

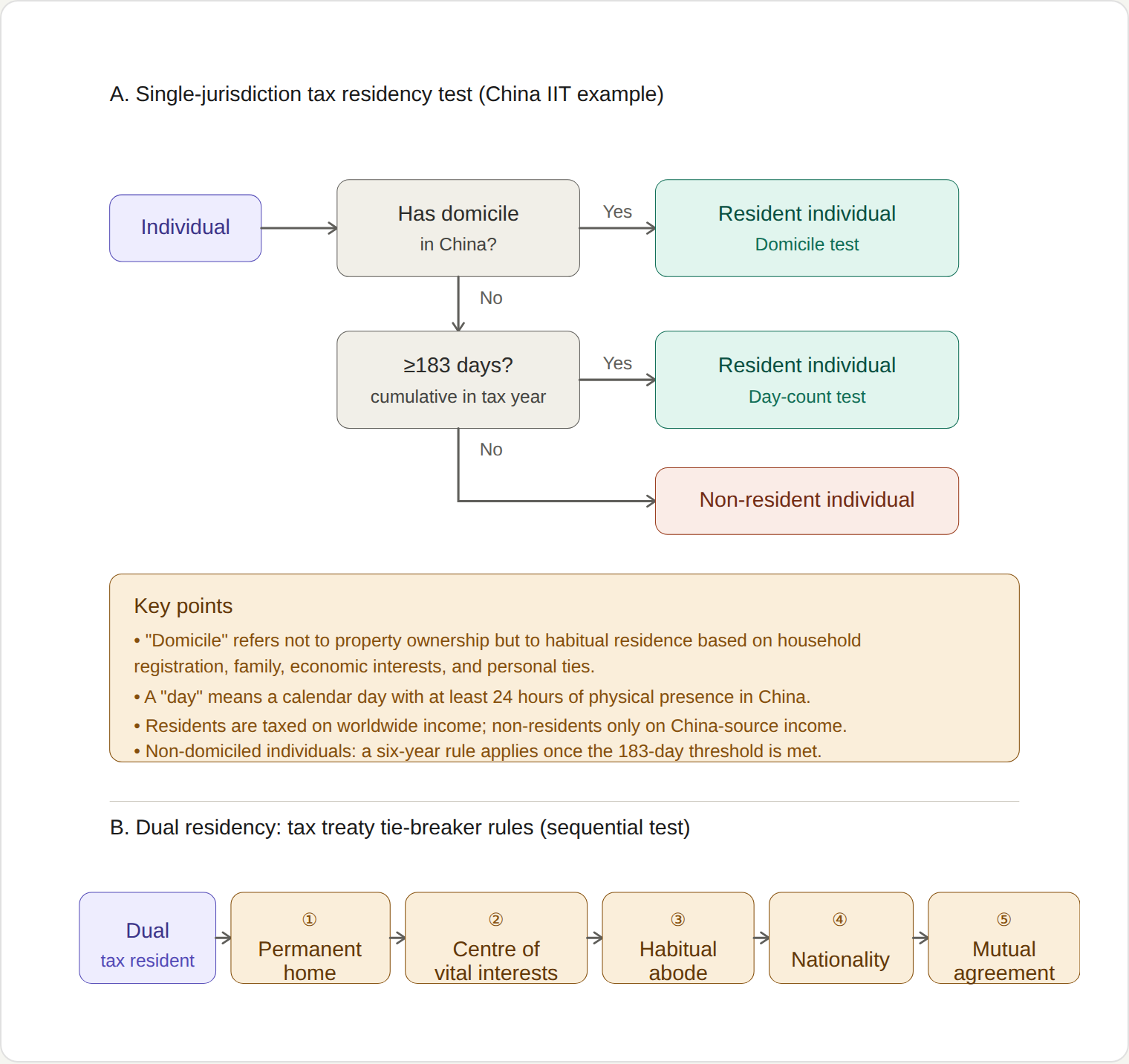

According to Article 1 of the Individual Income Tax Law, an individual who has a domicile within the territory of China, or an individual who does not have a domicile but has resided within the territory for a cumulative total of 183 days within a single tax year, is a resident individual. Between the two standards, the domicile standard holds a higher hierarchical position: only when an individual does not have a domicile within the territory will the number of days of residence be further examined.

Here, domicile is a fictitious concept in tax law and does not refer to whether one owns real estate. According to the Implementation Regulations, it refers to habitual residence within the territory of China due to household registration, family, and economic interest relations; even if an individual temporarily resides outside the territory for reasons such as study, work, or visiting relatives, as long as they will return to reside within the territory after these reasons conclude, the territory constitutes their habitual residence, which also means they have a domicile within the territory. Therefore, a Chinese citizen who works overseas for a long time but whose family and main economic interests remain within the territory may still be recognized as a resident individual with a domicile.

For individuals without a domicile, there are several details to note regarding the calculation of residence days: only a full 24 hours of stay within the territory on a given day is counted towards the number of days of residence in the territory, whereas stays of less than 24 hours are not counted; at the same time, the six-year rule exists—if an individual without a domicile has resided within the territory for a cumulative total of 183 days in a tax year for less than six consecutive years, or if there is a single departure exceeding 30 days in any given year during this period, their income sourced from outside the territory and paid by an overseas entity may be exempt from tax in China; if the period reaches six consecutive years without a single departure exceeding 30 days, starting from the seventh year, their overseas income shall also be included in the scope of taxation. This arrangement preserves a certain buffer space for individuals without a domicile who have been in China for a long term.

The determination logic of the U.S. has structural differences from that of China, placing more emphasis on identity nexus. U.S. citizens, regardless of where they reside, bear reporting obligations on their global income; non-citizens are mainly evaluated through two tests: the first is the green card test, where holding a valid green card constitutes a tax resident; the second is the substantial presence test, which calculates whether the threshold is met through a weighted calculation of the number of days stayed in the U.S.

The algorithm of the substantial presence test is worth elaborating as an illustrative example: the number of days stayed in the U.S. in the current year is fully counted, the previous year is calculated at one-third, and the year before that is calculated at one-sixth. If the three-year total reaches 183 days and the current year is no less than 31 days, the individual constitutes a tax resident. For example, if a person stays in the U.S. for 120 days each year for three consecutive years, the weighted calculation would be 120 + 40 + 20 = 180 days, which does not reach 183 days, and thus they are not considered a U.S. tax resident for that year. The meaning of 183 days is not the same under the Chinese and U.S. rules: the former is the cumulative number of days in a single year, while the latter is a weighted result across three years.

Precisely because the nexus adopted by different jurisdictions varies—some focus on domicile and time of residence, while others focus on nationality and residence qualifications—the exact same natural person can perfectly well be recognized as a tax resident by two jurisdictions simultaneously during the same period, thereby forming a dual resident status. The following table provides a brief comparison of the main criteria for determining individual tax resident status between China and the U.S. to illustrate the sources of these differences.

Table 1 Comparison of Main Criteria for Determining Individual Tax Resident Status between China and the U.S.

Data Source: Compiled based on the current tax laws of both jurisdictions and public information.

Dual resident status itself is not illegal, but if uncoordinated, it will lead to the same income being taxed repeatedly in both jurisdictions. The solution mainly relies on the conflict rules in tax treaties, detailed in Section 5.

According to Article 2 of the Enterprise Income Tax Law, a resident enterprise refers to an enterprise legally established within the territory of China, or an enterprise established in accordance with the laws of a foreign country (region) but whose place of effective management is located within the territory of China. China thereby adopts a determination principle that combines the place of incorporation standard with the place of effective management standard; the former is a formal standard, while the latter is a substantive standard. Those recognized as resident enterprises shall pay tax on all their income sourced from both inside and outside the territory; non-resident enterprises shall only pay tax on income sourced from within the territory, as well as on income that has an actual connection with their institutions or establishments within the territory.

The place of effective management refers to an establishment that exercises substantive and comprehensive management and control over the production and business operations, personnel, accounting, properties, etc., of an enterprise. For Chinese-controlled enterprises registered overseas, the State Taxation Administration has provided more detailed determination requirements in Guo Shui Fa [2009] No. 82: the places where senior management personnel perform their duties are mainly located within the territory; financial and human resource decisions are made by institutions or personnel within the territory or require their approval; major properties, accounting books, seals, and minutes of board and shareholder meetings are kept within the territory; and more than half of the directors or senior executives with voting rights habitually reside within the territory. This document simultaneously established the judgment principle of substance over form.

This means that if a company registered overseas has its true decision-making and management center located within the territory, it may still be determined to be a Chinese resident enterprise, and thereby pay tax in China on its global income. The choice of the place of incorporation itself cannot simply determine tax resident status.

Using the place of incorporation plus the place of effective management as dual standards is consistent with the universally adopted international practice of combining the place of incorporation and the place of effective management. This arrangement balances formal certainty with substantive fairness, and also provides a common language foundation for utilizing tax treaties to resolve dual resident issues of cross-border enterprises.

When an individual simultaneously constitutes a tax resident of two contracting parties, their single resident status needs to be determined in accordance with the tie-breaker rule in the tax treaty. Taking the OECD Model Tax Convention and the treaties signed by China with other countries as examples, the tie-breaker rules are applied step-by-step in a fixed sequence: first, look at the permanent home; when there is a permanent home in both sides, look at the center of vital interests with which their personal and economic relations are closer; if the center of vital interests cannot be determined or they do not have a permanent home in either place, look at the habitual abode; next, look at nationality; if it still cannot be determined, it shall be resolved by mutual agreement between the competent authorities of both sides. Once a higher-level standard is sufficient to determine the attribution, the next-level standard is no longer applied.

Figure 1 provides a comprehensive overview of the above determination logic: Part (A) is the determination process for individual tax resident status under a single jurisdiction (taking Chinese law as an example), and Part (B) is the step-by-step application of the tie-breaker rules in the case of dual residency.

Figure 1 Illustration of Individual Tax Resident Status Determination and Tax Treaty Tie-Breaker Rules

Source: Compiled and drawn based on the Individual Income Tax Law and tax treaty tie-breaker rules.

Determination of Individual Tax Resident Status

Case 1: A Chinese citizen dispatched overseas whose family and main economic interests remain within the territory

Facts: A is a Chinese citizen dispatched by a domestic enterprise to work permanently in a Southeast Asian country, residing overseas for more than 300 days throughout the year; A’s spouse and children, self-owned housing, and main investments are all within the territory of China, and A will return to reside within the territory after the dispatch ends.

Analysis: According to Article 1 of the Individual Income Tax Law, having a domicile within the territory constitutes a resident individual; the Implementation Regulations define domicile as habitual residence within the territory due to household registration, family, and economic interest relations, and it does not take actual residence as the requirement. Although A is located overseas for a long time, A’s family and main economic interests are still within the territory, and after the relevant events conclude, A will return to reside within the territory, which constitutes having a domicile within the territory.

Conclusion: A is a Chinese tax resident (resident individual) and should declare and pay tax in China on all income sourced from both inside and outside the territory.

Case 2: A foreign individual who has resided in China for a cumulative total of 183 days

Facts: B is a foreign citizen without a domicile in China. Because B is employed by a domestic company, B resided within the territory of China for a cumulative total of 210 days in a certain tax year.

Analysis: For individuals without a domicile, Article 1 of the Individual Income Tax Law uses time of residence as the standard: those who reside within the territory for a cumulative total of 183 days within a tax year are resident individuals. B has resided for a cumulative total of more than 183 days in that year.

Conclusion: B constitutes a Chinese tax resident in that tax year; however, whether all of B’s overseas income is included in taxation still needs to be judged in conjunction with the six-year rule (see Case 5).

Case 3: A foreign individual on a short-term visit to China, residing for less than 183 days

Facts: C is an overseas resident who has visited China multiple times for short-term projects, residing within the territory for a cumulative total of 120 days throughout the year, and has no domicile within the territory.

Analysis: C neither has a domicile within the territory, nor has C resided for a cumulative total of 183 days in that year. Neither of the two standards for a resident individual is met.

Conclusion: C is a non-resident individual and only pays tax in China on income sourced from within the territory of China.

Case 4: Calculation of residence days: Full 24 hours and borderline situations

Facts: D is an individual without a domicile who frequently travels back and forth between inside and outside the territory; D has entered and exited on the same day multiple times, and also had several cross-day stays where the stay on a single day was less than 24 hours.

Analysis: According to the relevant regulations on the determination of residence time for individuals without a domicile, only a full 24 hours of stay within the territory on a given day is counted towards the number of days of residence in the territory; stays of less than 24 hours are not counted. D’s same-day round trips and stays of less than 24 hours are not counted. The recalculated residence days based on this may differ significantly from the results calculated by calendar days, and will directly impact the judgment of whether D has met the 183-day threshold.

Conclusion: Residence days should be calculated day-by-day based on the full 24-hour criteria; individuals with borderline days should retain complete entry and exit records to support status determination.

Case 5: Long-term foreign individuals in China and the six-year rule

Facts: E is a foreign individual who has resided within the territory for at least 183 days every year since 2019. Scenario One is that there was no single departure exceeding 30 days during the six years; Scenario Two is that there was one departure lasting 45 days in one of the years during this period.

Analysis: According to Announcement No. 34 of 2019 by the Ministry of Finance and the State Taxation Administration, for an individual without a domicile who has resided within the territory for a cumulative total of 183 days in a tax year for six consecutive years without any single departure exceeding 30 days, their overseas income shall also be subject to Chinese taxation starting from the seventh year; if they reside for less than 183 days in any year or have a single departure exceeding 30 days, the consecutive years are recounted, and their income sourced outside the territory and paid by an overseas entity can be exempt from tax in China. Under Scenario One, E should pay tax on global income starting from the seventh year; under Scenario Two, because that departure exceeded 30 days, the consecutive years are recounted, and overseas income paid overseas is still exempt from tax.

Conclusion: The application of the six-year rule highly depends on the number of residence days year-by-year and the duration of a single departure. E’s tax obligations on overseas income are completely different under the two scenarios.

Case 6: An individual who has only obtained foreign permanent residency but whose center of life is within the territory

Facts: F has obtained permanent residency in a certain country (commonly known as a green card), but F’s family, work, and main source of income are all within the territory of China, and F primarily resides within the territory throughout the year.

Analysis: Permanent residency is a residency qualification under immigration law, which belongs to a different category from tax resident status. One cannot be determined as a non-Chinese tax resident solely based on holding foreign permanent residency; status determination should still return to the tax law standards regarding domicile and time of residence. F’s center of life is within the territory, constituting a domicile within the territory.

Conclusion: F remains a Chinese tax resident; when making a tax resident status self-certification at financial institutions, F should truthfully declare their Chinese tax resident status.

Determination of Enterprise (Entity) Tax Resident Status

Case 7: An enterprise established in accordance with domestic laws (Place of incorporation standard)

Facts: Company G was registered and established within the territory in accordance with Chinese laws, and its business activities are mainly carried out within the territory.

Analysis: Article 2 of the Enterprise Income Tax Law stipulates that an enterprise legally established within the territory of China is a resident enterprise. The place of incorporation standard is a formal standard. Any enterprise legally established within the territory belongs to resident enterprises, without the need for further examination of the place of effective management.

Conclusion: Company G is a resident enterprise and should pay enterprise income tax on all its income sourced from both inside and outside the territory.

Case 8: A Chinese-controlled enterprise registered overseas with its place of effective management within the territory

Facts: Company H is controlled by a domestic enterprise group and registered overseas in accordance with foreign laws; the places where its senior management personnel perform their duties, financial and human resource decisions, main properties and accounting books, and minutes of board and shareholder meetings are all within the territory of China, and more than half of the directors with voting rights habitually reside within the territory.

Analysis: According to Article 2 of the Enterprise Income Tax Law and Guo Shui Fa [2009] No. 82, if a Chinese-controlled enterprise registered overseas simultaneously meets the requirements regarding the place of duty performance, place of decision-making, storage of main properties and important documents, and residence of directors and senior executives, it should be recognized as a resident enterprise whose place of effective management is within the territory (a non-domestically registered resident enterprise) in accordance with the principle of substance over form. Company H meets all the above requirements.

Conclusion: Company H is recognized as a Chinese resident enterprise and should pay tax in China on all its income sourced from both inside and outside the territory.

Case 9: An enterprise registered overseas with its place of effective management overseas

Facts: Company I is registered overseas in accordance with foreign laws. Its management decisions, personnel, and accounting books are all overseas, and it only obtains some royalty income within the territory of China.

Analysis: Company I was neither established in accordance with domestic laws, nor is its place of effective management within the territory, so it does not constitute a resident enterprise; it only pays tax on income sourced from within the territory, as well as on income that has an actual connection with its institutions or establishments within the territory.

Conclusion: Company I is a non-resident enterprise and only pays tax in China on its income sourced from within the territory of China (such as this royalty income).

Dual Resident Status and Tax Treaty Tie-Breaker Rules

Case 10: Dual resident of the Mainland and Hong Kong: Attribution determined by permanent home

Facts: J has worked in Hong Kong for a long time, rents a residence, and J’s family has settled in Hong Kong, but J’s Mainland household registration has not been canceled. J may be recognized as a resident under both Mainland and Hong Kong tax laws.

Analysis: According to the tie-breaker rule introduced in the Arrangement between the Mainland of China and the Hong Kong Special Administrative Region for the Avoidance of Double Taxation and the Prevention of Fiscal Evasion with respect to Taxes on Income, the permanent home should be compared first. J has a residence for long-term living in Hong Kong, constituting a permanent home; J only retains a household registration in the Mainland without a place for long-term living, so it is difficult to say J has a permanent home. The attribution can be determined at the first step, without the need to proceed to subsequent standards.

Conclusion: J should be determined as a Hong Kong tax resident.

Case 11: Permanent homes in both sides: Determined by the center of vital interests

Facts: K has maintained long-term residences in both the Mainland and a certain overseas country; K’s family is mainly overseas, but K’s main business operations, directorships, and main sources of income are in the Mainland.

Analysis: When an individual has a permanent home in both sides, the tie-breaker rule proceeds to the second step, which is comparing the center of vital interests with which their personal and economic relations are closer. Judgment requires a comprehensive consideration of personal relations and economic relations: K’s center of economic interests is in the Mainland, while family relations lean overseas. When the two directions are inconsistent, an overall weighing of their personal and economic ties should be made.

Conclusion: If comprehensive judgment determines that K’s center of vital interests is in the Mainland, K should be determined as a tax resident of the Mainland (China); this determination belongs to a case-by-case weighing, and if necessary, it is determined through mutual agreement by the competent authorities of both sides.

Case 12: Center of vital interests difficult to determine: Retracting to habitual abode and nationality

Facts: L has residences in both countries, and L’s personal relations and economic relations are roughly balanced, making the center of vital interests difficult to determine.

Analysis: If the center of vital interests cannot be determined, or the individual does not have a permanent home in either place, the tie-breaker rule retracts to the third step, habitual abode, and then to nationality; if it still cannot be determined, it is resolved through mutual agreement by the competent authorities of both sides. As for L, L’s usual primary place of residence should be examined sequentially, followed by L’s nationality.

Conclusion: L’s resident status should be determined step-by-step in the order of habitual abode and nationality, and if necessary, a single attribution will be determined through consultation by the competent authorities.

Case 13: A U.S. green card holder residing overseas

Facts: M holds a U.S. green card but has settled long-term in a certain country that has signed a tax treaty with the U.S., and constitutes a tax resident of that country.

Analysis: According to U.S. rules, a green card holder is in principle a U.S. tax resident and must declare global income. As a dual tax resident, M can claim to be recognized as a resident of the other contracting party in accordance with the treaty resident clause (tie-breaker rule), thereby being treated as a non-resident in the U.S. However, M must follow the procedures to notify the U.S. tax authorities in advance, and this choice may affect the maintenance of M’s green card status.

Conclusion: M can be recognized as a U.S. non-tax resident via the treaty tie-breaker rule, but must fulfill corresponding reporting procedures and weigh its potential impact on residency status.

Tax Resident Status Determination in the Context of Tax Information Transparency

Case 14: Holding an overseas passport but ordinarily residing within the territory: Overseas account information exchanged via CRS

Facts: N holds an overseas passport but has resided long-term within the territory of China. Both N’s life and economic centers are within the territory, and N holds accounts in overseas financial institutions (including accounts held through offshore companies).

Analysis: The determination of tax resident status is subject to tax law standards rather than passports. N’s center of life is within the territory, so N may still constitute a Chinese tax resident. Under the CRS framework, financial institutions identify the tax resident status of the account holder (or the actual controller if the account holder is a passive non-financial entity) through tax resident status self-certification and look-through verification, thereby deciding the direction of information reporting. Once identified as a Chinese tax resident, the relevant account information will be exchanged back to China.

Conclusion: There is a possibility that N’s overseas account information will be exchanged back to China; N should truthfully make a tax resident status self-certification and fulfill the obligation to declare overseas income.

Case 15: CRS reporting for dual residents: Reporting all tax residencies

Facts: O simultaneously constitutes a tax resident of two jurisdictions and holds financial accounts overseas.

Analysis: After the revised CRS 2.0 implementation, an account holder with dual tax resident status should declare all their tax resident jurisdictions in the self-certification. Financial institutions will report to all their resident jurisdictions and no longer apply the previous practice of selectively reporting to one jurisdiction under a treaty. O must not selectively declare only one jurisdiction.

Conclusion: O should truthfully declare all of O’s tax resident statuses, and the relevant account information will be exchanged to all of O’s resident jurisdictions.

It should be added that not all treaties directly state the tie-breaker rules explicitly. For example, the China-U.S. tax treaty only stipulates that dual residency shall be determined by mutual agreement between the competent authorities of both sides, but in practice, it is usually still handled by referencing the tie-breaker rules; a U.S. green card holder residing in another country can also be recognized as a U.S. non-tax resident in accordance with the resident clause of the treaty, provided they must follow procedures to notify the U.S. tax authorities in advance, and this action may affect the maintenance of their green card status.

The significance of tax resident status is further magnified under the CRS framework. CRS was introduced by the OECD in 2014, signed and joined by China in 2015, and completed its first information exchange in September 2018; it currently covers over 100 jurisdictions. Under this mechanism, financial institutions require clients to make a tax resident status self-certification at the account opening stage, and perform look-through verification on accounts held by offshore companies to identify the tax resident status of their actual controllers, thereby deciding to which jurisdiction the account information should be reported.

CRS 2.0 further tightened the handling of dual residents: previously, dual tax residents were allowed to selectively report to a single jurisdiction based on treaties in their self-certifications; after the revision, they are required to declare all tax resident jurisdictions, and financial institutions need to report to all their resident jurisdictions, no longer applying selective reporting. This change means that the judgment of tax resident status is not only the prerequisite for the tax administration of overseas income, but also directly determines the flow of financial account information; a deviation in status judgment may simultaneously bring about compliance risks at the levels of reporting omission and information exchange.

Looking at the entire text, the determination of tax resident status can be summarized into several main threads: for individuals, the domicile standard comes first, supplemented by the time of residence standard, and accompanied by the six-year rule and detailed rules for counting days; for enterprises, the place of incorporation is combined with the place of effective management, prioritizing substance over form; when dual residency occurs, a single attribution is determined step-by-step by the tie-breaker rules of tax treaties; and under the background of CRS information transparency, status determination has become a prerequisite step for cross-border tax compliance.

For cross-border individuals and enterprises, the following points can be considered. Firstly, accurately judge and periodically review one’s own tax resident status, avoiding simple substitution of tax law judgment with nationality or residency qualifications. Secondly, pay attention to retaining evidence such as residence days, entry and exit records, and activity trajectories, to prepare for the needs of status determination and day calculation. Thirdly, when dual residency is involved, the applicable tax treaties and tie-breaker rules should be promptly invoked, and filings or applications should be handled according to regulations. Fourthly, enterprises should pay attention to the actual layout of their places of effective management, avoiding resident status risks caused by a mismatch between the place of incorporation and the management center. For situations with complex structures or significant amounts, it is advisable to seek professional advice in advance.

FinTax offers crypto accounting suite, tax calculator and professional tax consulting services.